Olo: Pioneering the Digitization of Restaurant Ordering

In this article we will cover Olo and give some insight into what they do, and where we think they are headed.

Hey everyone, welcome to TheTechBruin where we break down companies and subverticals within technology. At the end of each article, we will give our thoughts about the company/vertical and where we think it is headed. We will try to release a new article every week and hope you guys enjoy!

DISCLAIMER: None of this is investment advice and we are by no means experts. We are simply college students writing to further our technology industry knowledge.

Table of Contents

Company Context

Business Overview

Competitive Landscape

Pros and Cons of the Business

Key Metrics

Future Outlook

Company Overview

Many of you have probably ordered from Panda Express or Wingstop through their online platforms, hoping your food would be ready upon arrival. What you might not realize is that behind many of these late-night fast food orders is Olo, the company making it all possible.

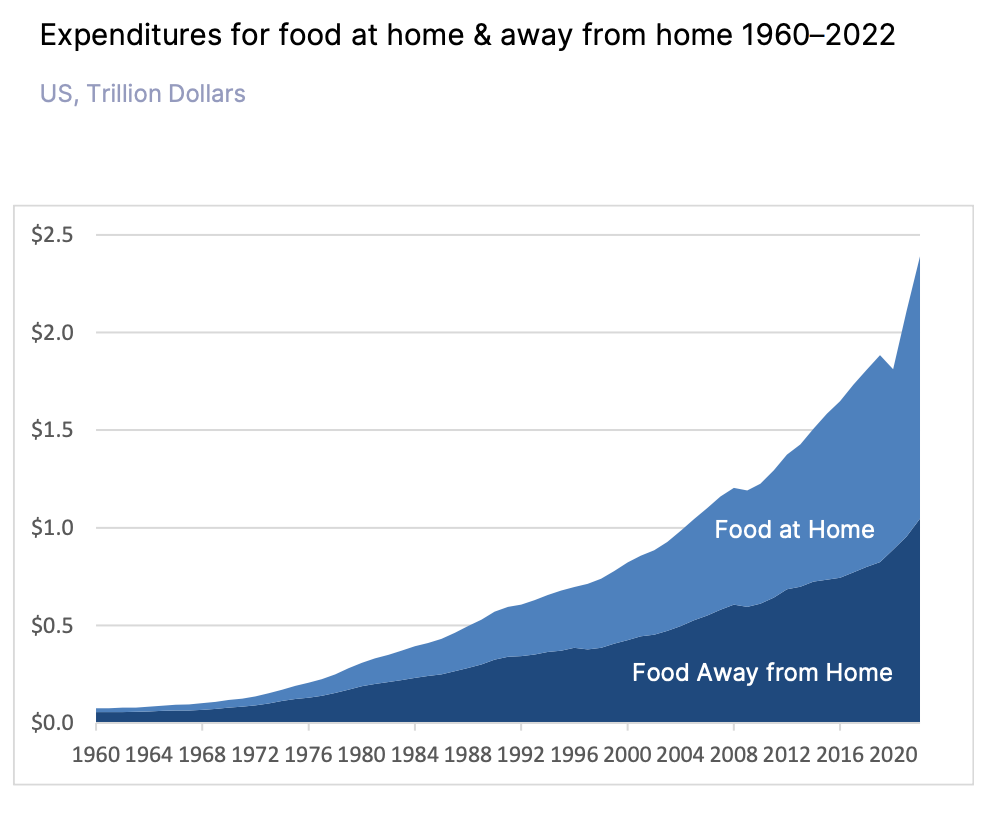

Olo is a vertical software company in the restaurant industry, focused on digitizing food ordering for major fast food and restaurant chains like Wingstop and Five Guys. In every investor presentation, they emphasize that “only 16% of restaurant orders are online.” They also highlight the growing demand within the “food away from home” market, which surpassed “food at home” demand during the COVID-19 pandemic, presenting this market as their growth opportunity.

Business Overview

Olo hosts delivery, pickup, and mobile order websites for franchises, allowing them to customize these websites to their preferences. They also manage email CRM campaigns, customer data analytics, and table hosting. Additionally, through their extensive partnerships with many Payment companies and digital ordering aggregators, they have expanded into the payments and third-party aggregation business themselves.

Olo’s business model is based on a “transactional SaaS” framework, deriving revenue from subscriptions and transactions.

Breaking Down Olo’s Subscription Services

Subscription revenue comes from selling their “modules” or individual services, including Ordering, Switchboard, Kiosk, Virtual Brands, Marketing Sentiment, Guest Data Platform, and Host. Customers can use any number of these modules, and the more they use, the higher the subscription fee, similar to many “land and expand” SaaS models.

Subscription Modules:

Ordering: Manages all incoming orders and collects customer information for restaurant use.

Switchboard: Streamlines phone ordering by outsourcing orders to call agents or restaurant employees, providing an easy-to-use interface.

Kiosk: Uses in-store kiosk partnerships combined with Olo Pay to give customers a more accurate ordering timeline.

Virtual Brands: Helps brands without a physical presence manage mobile and delivery orders using the Rails and Dispatch modules.

Marketing Sentiment: Assists enterprises with CRM and digital campaigns.

Guest Data Platform (GDP):** Uses order and transaction data to power marketing campaigns, analytics, or other informational needs.

Host: Digitizes reservation management for stores.

Transactional Revenue Streams

On the transactional side, revenue is gained through the Rails, Dispatch, and the Pay module.

Rails: Synchronizes menu items to third-party marketplaces like Uber Eats or Grubhub, earning revenue from each order.

Dispatch: Does the same thing as Rails does, but for delivery services, allowing customers to outsource delivery to third-party apps and earn a percentage of the transaction.

Olo Pay: This allows Olo to pocket a small percentage of each transaction run through the module. This is achieved by partnering with companies throughout the payment process (Gateways, Acquirers, and Processors).

Competitive Market Landscape

The restaurant software and technology space is extensive, so the competition can be broken down by segment as it is relevant to Olo. All companies listed below have been directly listed on the Olo 10-K as competitors as of the end of 2023.

White-Label Ordering: Olo’s main competitors are Paytronics, Tillster, and Lunchbox. White-label ordering involves outsourcing the hosting of an ordering website while keeping the brand’s logo. This segment is by far the most threatening segment to Olo’s core business as these businesses have almost identical offerings to Olo.

Restaurant POS Systems: Olo faces competition from companies like NCR Voyix, Toast, Square, PAR Technology, QU POS, and Revel. Although Olo does not maintain its own POS system and relies on partnerships, these companies can serve as competition when not integrated with Olo Pay. Olo has partnered with Toast, Square, and other POS systems to allow customers to view orders directly through these systems but can’t take advantage of these partnerships until the customer opts into the Olo Pay program.

Digital Online Aggregators: Aggregators like Grubhub, UberEats, and Doordash can sometimes take order volume away from Olo, although they are partners through the Rails and Dispatch modules. If a company opts for these modules and receives orders through these aggregators, it benefits Olo.

Third-Party Aggregators: Competitors include Checkmate.com and Deliverect, which directly compete with Olo’s Rails and Dispatch modules.

Payment Services: In payments, Olo’s partnership with POS gateways and processors like Adyen is beneficial, but other companies within the payments sector still compete with Olo’s offerings when not integrated within the Olo Pay ecosystem. And once again, if the company does not opt in for the Olo Pay module, these partnerships don’t benefit Olo at all.

Data Platforms: Olo competes with firms offering omnichannel analytics, specifically naming Twilio’s data platform segment and mParticle as direct competitors.

Table Hosting: Competitors include OpenTable and Yelp.

Olo’s Pros & Cons

Pros:

It is an end-to-end platform for customers managing restaurants under one software system.

Diverse partnerships allow Olo to capture market share as customers use legacy payment and kiosk systems through their Pay module instead of as a stand-alone product.

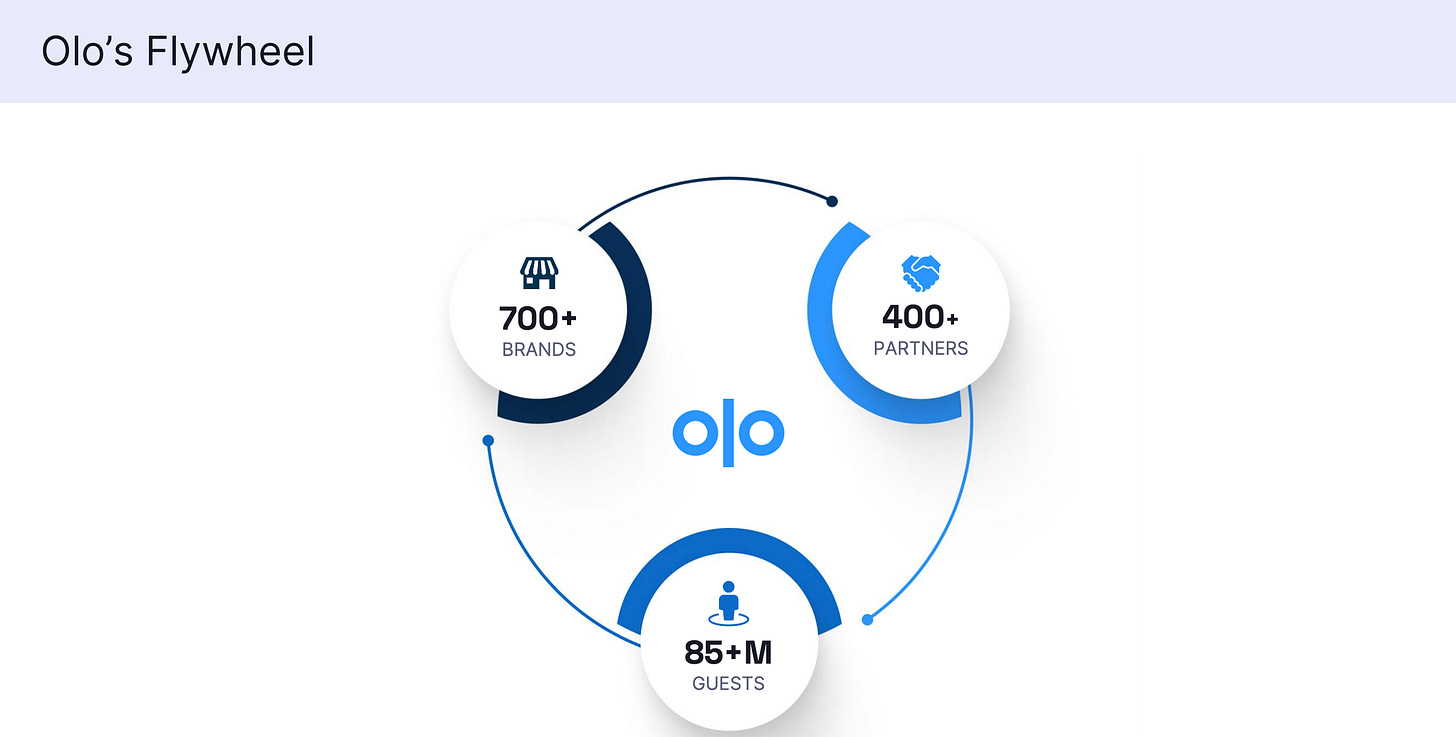

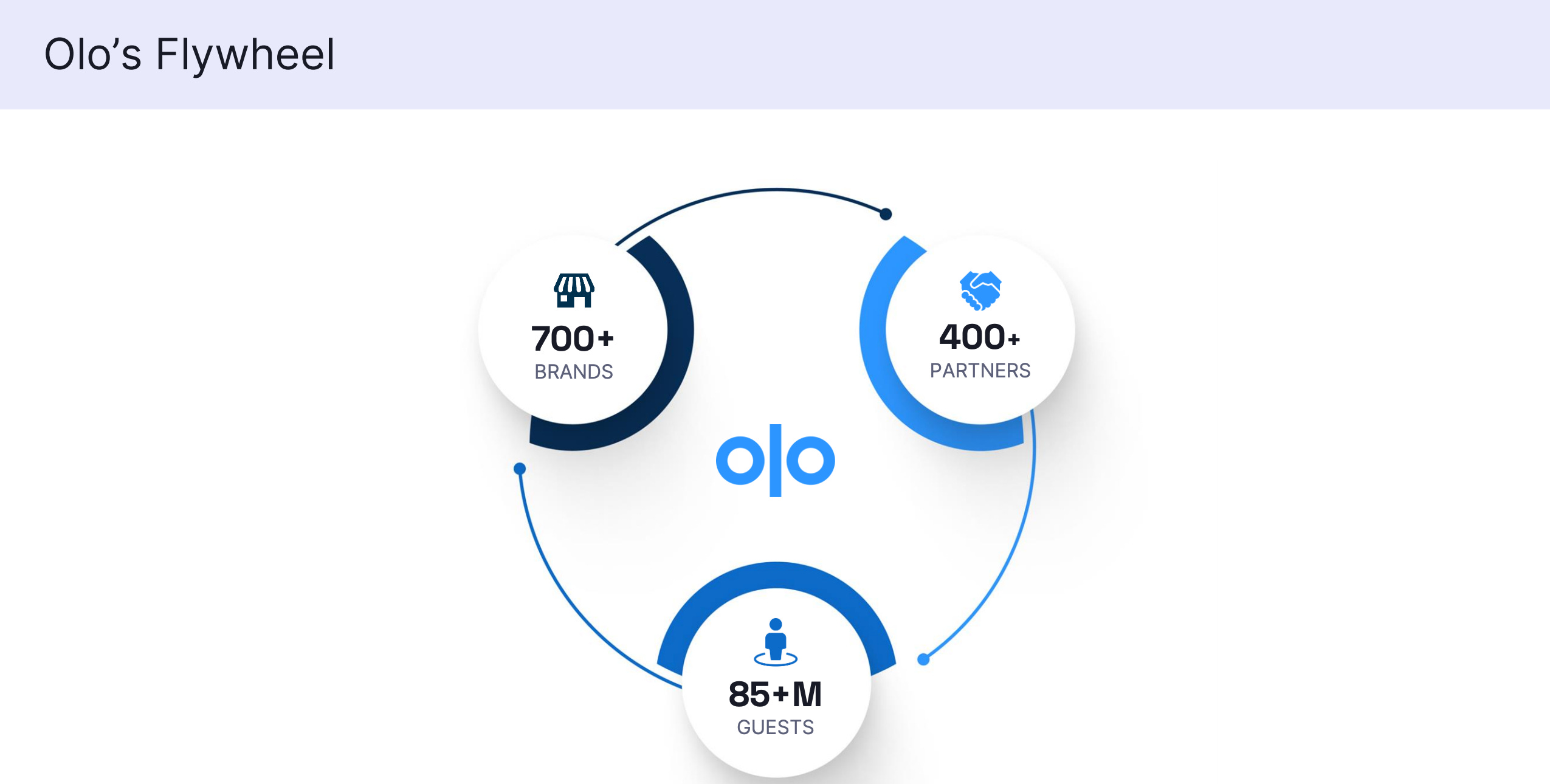

Their Flywheel GTM strategy emphasizes devotion to their customers, contributing to high retention rates.

2024 Q2 Investor Presentation

Cons:

A high price tag reduces the likelihood of SMB restaurants using Olo. They don’t specify exactly how much they charge as it changes based on their own internal evaluation of the customer.

Customers cannot cancel orders, leading to notable frustration.

Olo’s reputation sets it apart from competitors like ChowNow and Lunchbox.io. Additionally, partnerships with major payment platforms give Olo an edge for a more seamless offering. These other white-label ordering companies are smaller with similar offerings, so Olo’s reputability and brand name keep it at the industry’s forefront.

Key Metrics

Currently, Olo operates in 82,000 restaurants (an increase of 5,000 since Q2 2023) and has added about 100 brands over the past year.

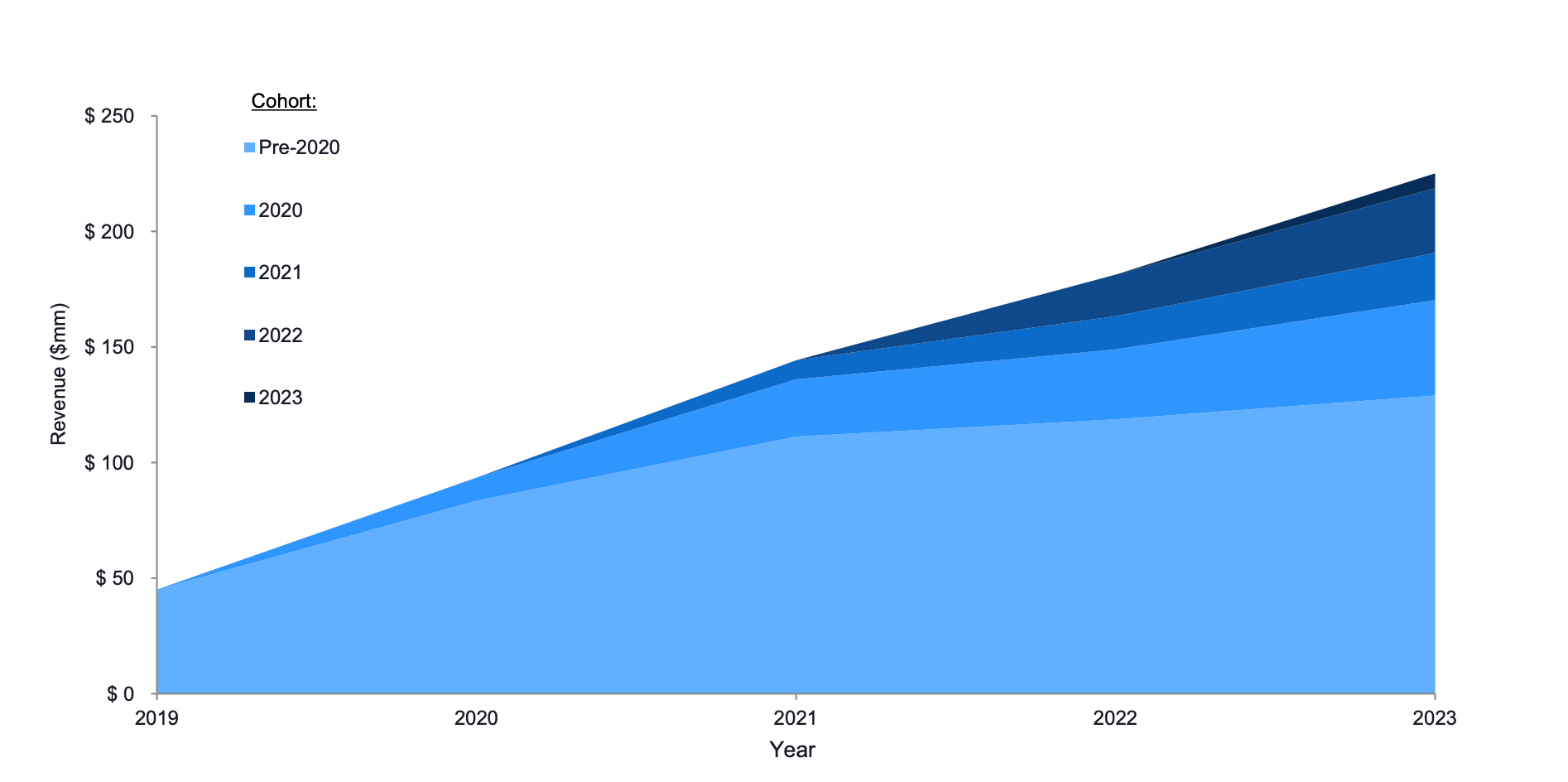

Total revenue increased by 28.5% YoY to $70.5 million, with platform revenue growing 27% YoY to $69.6 million. Platform revenue accounted for 98.7% of total revenue, with the remaining 1.3% from professional services and other unspecified streams. GMV jumped by $3B+ to $26B, and GPV exceeded $1B for the first time. Their LTV for all cohorts is shown in the image below.

Gross profit increased by 16% YoY to $39.5 million, 57% of total revenue, although gross margins have been declining since 2021. Operating income was $1 million (1% of revenue) compared to a $21.2 million loss in Q2 2023. Net income was $5.7 million, or $0.03 per share, compared to a Q2 2023 net loss of $17.1 million, or $0.11 per share.

ARPU (Average Revenue Per Unit) increased by 19% YoY to $852. NRR was over 120% for the second consecutive quarter, higher than in Q2 2023. These metrics indicate customer affinity for Olo’s platform and their willingness to spend more on the service.

Future Outlook

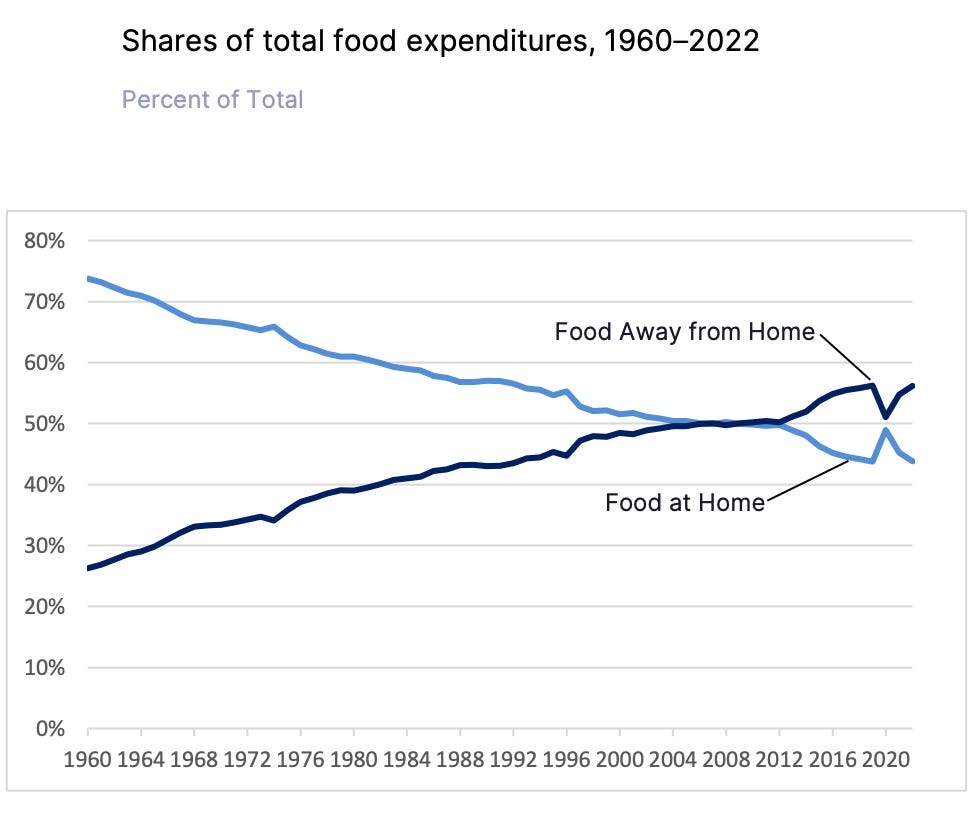

Olo has a promising future. Their product seems to stick very well with customers and their TAM keeps increasing YoY. As the percentage of spending on eating out (56%) has overtaken spending on eating at home (44%), Olo has significantly boosted its Gross Merchandise Value (GMV) by expanding to more restaurants. Additionally, with 69% of all dining-out sales coming from full-service and fast-food restaurants, Olo is well-positioned to grow its business by capitalizing on this trend of increased dining out.

They are also trending towards becoming a full-stack payment platform through their growing list of payment partnerships, emphasizing that Olo Pay will be the fastest-growing module in the coming year. Their retention has remained steady due to continued investment in their modules and customers, indicating they are not losing customers to other third-party aggregators or white-label ordering platforms.

I expect Olo to maintain strong revenue growth, as they have since their IPO. Additionally, as they mature, operating expenses should trend down as a percentage of revenue, expanding operating margins.

My initial concern was the downward trend in gross margins (from >80% to 57% from 2021 to 2024). However, Olo attributes this to increased locations resulting in higher hosting and compensation costs, or for 2023, increased adoption of Olo Pay resulting in more processing costs. This shrinking gross margin isn’t necessarily negative as it has fueled substantial growth. The gross margin has rebounded slightly in the last two quarters, and I hope to see this trend continue as the company matures.

Overall, Olo is a great company led by great people and is a pioneer in the restaurant SaaS space. I believe they will continue to grow, albeit at a diminishing rate, as more players enter with similar offerings but will increase profitability as growth diminishes over the next decade.

That’s all for this week. I hope you guys enjoyed this quick summary of Olo and please feel free to reach out to us if you would like to discuss any material in the article further.

Email: thetechbruin@gmail.com

Twitter/X: @TheTechBruin